Weekly Market Report (February 24, 2025) - Insights and Forecasts

Dive into the market analysis for February 24, 2025, covering SPY, QQQ, IWM, and the week’s key economic data. Stay ahead with expert insights and forecasts.

Weekly Market Report for February 24, 2025

On Monday, the markets remained closed in observance of President's Day. Earlier in the week, the S&P 500 reached a new record high of 6,147, buoyed by limited selling pressure and a readiness to buy on any dip.

However, by the end of the week, the tone shifted as profit-taking led to a consolidation trade. Concerns over valuations and a slowdown in momentum among some of the top year-to-date performers sparked speculation that the market might be peaking in the near term, which in turn dampened buying activity.

Additional growth worries emerged after Friday’s economic reports. The preliminary February S&P Global US Services PMI slipped into contraction territory (falling below 50), the final University of Michigan Consumer Sentiment Index for February dropped to 64.7, and existing home sales fell by 4.9% month-over-month in January.

Lackluster fiscal Q1 and full-year guidance from Walmart (WMT) also contributed to the increased selling pressure later in the week.

Both mega cap and small cap stocks experienced the steepest declines, while the rest of the market performed relatively better. Specifically, the market-cap weighted S&P 500 fell by 1.7% from last Friday; the equal-weighted S&P 500 dropped by 0.7% over the week; the Russell 2000 declined 3.7%; and the Vanguard Mega Cap Growth ETF (MGK) fell by 2.7%.

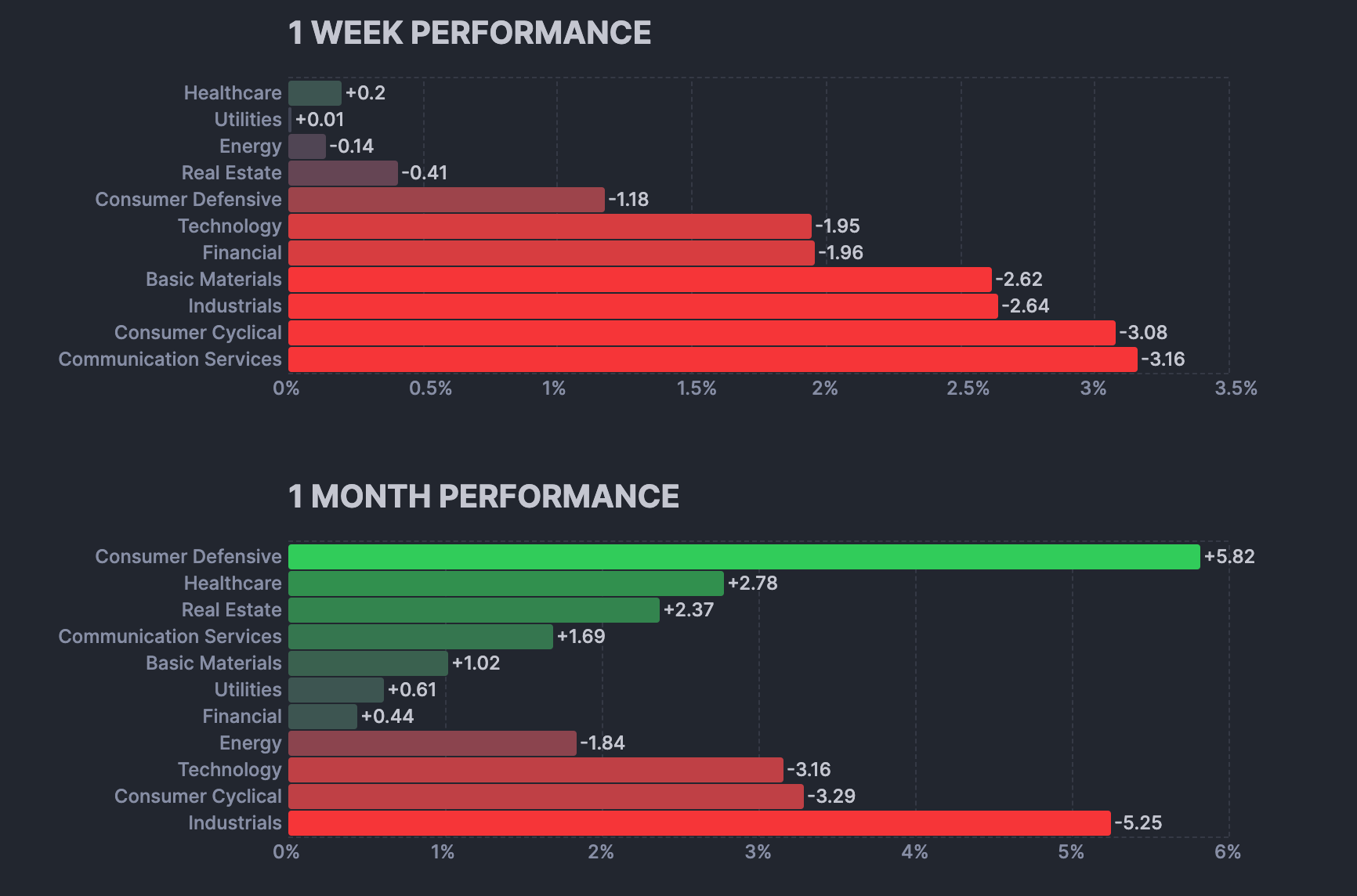

Weakness in the mega cap arena was evident in the S&P 500 consumer discretionary (down 4.3%) and communication services (down 3.7%) sectors—both of which include many large-cap stocks—registering the most significant losses among the 11 sectors. In contrast, defensive sectors such as utilities (+1.4%), consumer staples (+0.9%), and health care (+1.1%) were among the top performers.

Amid ongoing tariff discussions, market participants largely viewed tariffs as a bargaining chip rather than a permanent measure. President Trump announced that the auto tariff rate would be around 25% starting April 2 and indicated that tariffs on pharmaceuticals and semiconductors were also under consideration.

For the week, the indices recorded the following changes:

Dow Jones Industrial Average: -2.5% for the week / +2.1% YTD

S&P 500: -1.7% for the week / +2.2% YTD

Nasdaq Composite: -2.5% for the week / +1.1% YTD

S&P Midcap 400: -3.0% for the week / -0.6% YTD

Russell 2000: -3.7% for the week / -1.6% YTD

Weekly Market Heatmap

Weekly Sector Performance

Looking Ahead to the Upcoming Week

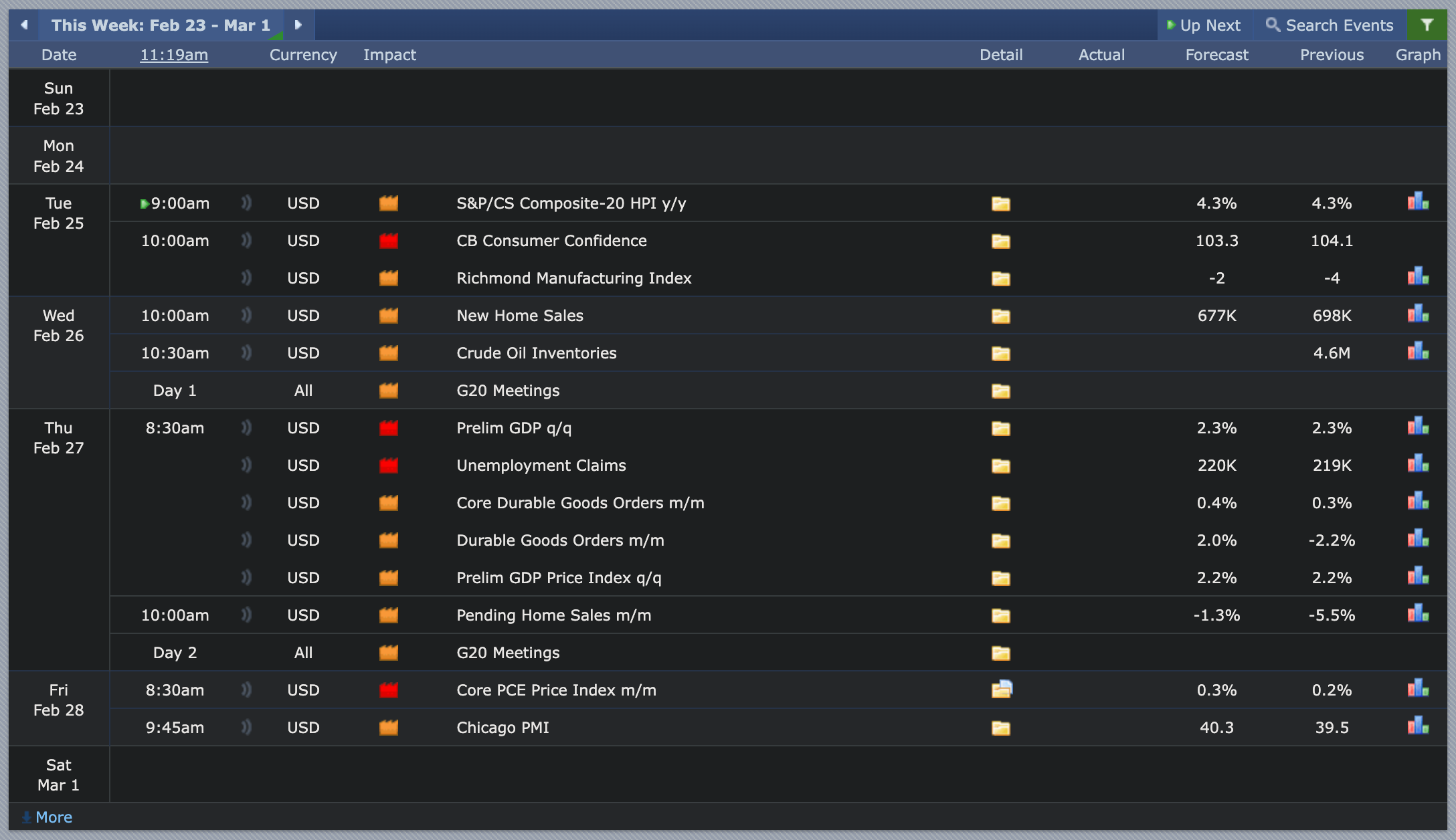

Next week features a busy slate of economic reports and corporate earnings that could sway market sentiment. On the economic front, investors will watch the Consumer Confidence reading, the Richmond Manufacturing Index, and new home sales for insights into consumer and housing trends. Later in the week, preliminary GDP and core PCE price index figures—key indicators for growth and inflation—will be in focus, alongside G20 meetings that may touch on global trade issues.

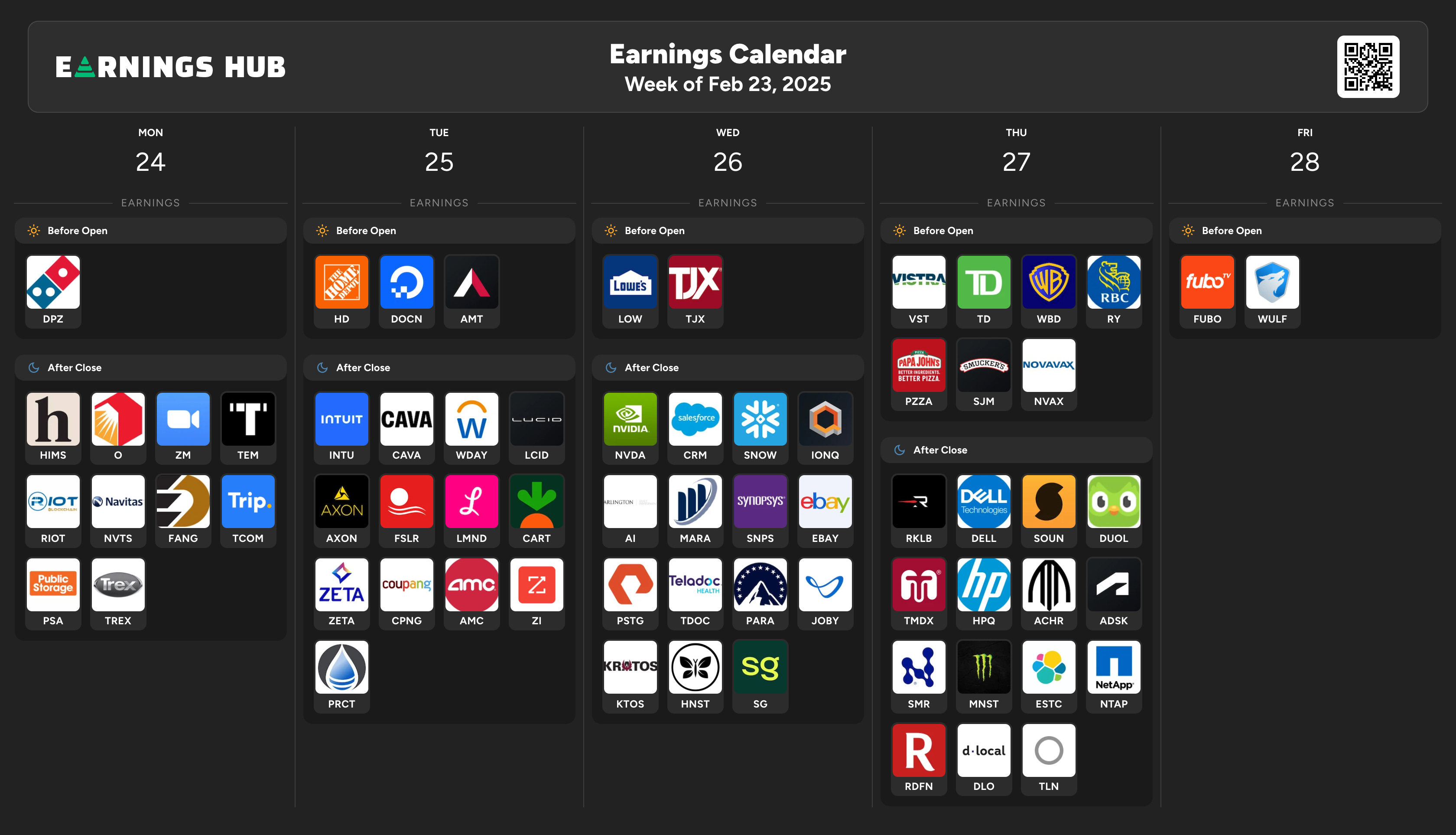

On the earnings side, retailers (such as Lowe’s, TJX, and Target) will offer updates on consumer spending and inventory management, while tech names (including Salesforce, Roku, and Zoom) will provide a view of enterprise and streaming demand. Toward the end of the week, companies like Alibaba, Dell, and Costco will round out the lineup, giving a broad look at both global e-commerce and U.S. consumer behavior. Overall, these announcements and data releases should give investors fresh clues about economic momentum and corporate performance heading into March.

Economic Events

Earnings Event

Market Health

The market currently is in a sell mode.

Broader Market - SPY, QQQ, IWM, MDY

On the weekly timeframe, SPY, QQQ, IWM, and MDY all appear to be in longer-term uptrends but are showing signs of waning momentum. Price action remains above key moving averages, reflecting an overall bullish structure, yet the momentum indicator hints at possible near-term fatigue or consolidation. While no major support levels have been decisively broken, the recent flattening of momentum suggests traders should watch for a pullback or extended consolidation phase before any renewed push higher.

Watch List

To be provided on X:

Disclaimer: This newsletter is not trading or investment advice, but for general informational purposes only. This newsletter represents our personal opinions that we share publicly for educational purposes. Futures, stocks, and bonds trading of any kind involves a lot of risks. No guarantee of any profit whatsoever is made. In fact, you may lose everything you have. So be very careful. We guarantee no profit whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission, CFTC, or with any other securities/regulatory authority. Consult with a registered investment advisor, broker-dealer, and/or financial advisor. By reading and using this newsletter or any of my publications, you are agreeing to these terms. Any screenshots used here are courtesy of ForexFactory, EarningsHub, Finviz, ThinkorSwim, and/or Tradingview. We are just end-users with no affiliations with them.