Weekly Market Report (February 16, 2025) - Insights and Forecasts

Dive into the market analysis for February 16, 2025, covering SPY, QQQ, IWM, and the week’s key economic data. Stay ahead with expert insights and forecasts.

Weekly Market Report for February 16, 2025

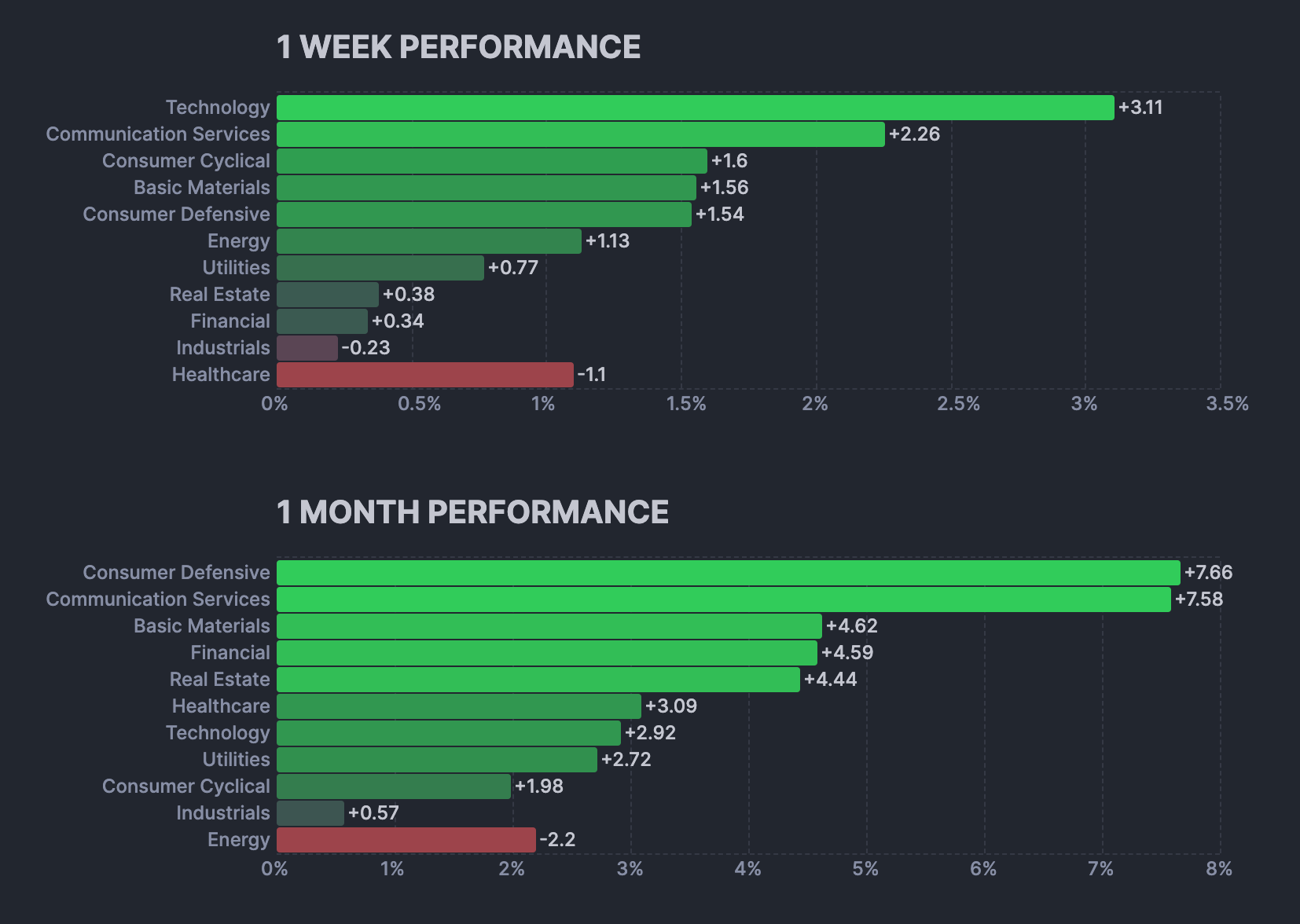

The major equity indices advanced this week, largely driven by strong gains in mega-cap stocks. The Vanguard Mega Cap Growth ETF (MGK) climbed 2.5%, while the market-cap weighted S&P 500 outperformed, rising 1.5% compared to the 0.5% gain in the Invesco S&P 500 Equal Weight ETF (RSP). Mega-cap strength was evident in sector performance, with the information technology sector leading at +3.8%, followed by communication services at +2.0%. Investors also digested a wave of economic data, trade developments, and Federal Reserve commentary. Fed Chair Powell’s semiannual testimony before Congress reaffirmed a cautious stance, reiterating that there is no urgency to adjust monetary policy. Meanwhile, President Trump imposed 25% tariffs on steel and aluminum, effective March 12, though Australia may receive an exemption. His reciprocal tariff plan, initially feared to be disruptive, turned out to be more measured, with implementation delayed until at least April 1 on a case-by-case basis.

Economic reports presented mixed signals. The New York Fed’s January Survey of Consumer Expectations showed stable one-year inflation expectations at 3.0%, but the University of Michigan’s February Consumer Sentiment Index reflected a sharp rise in year-ahead inflation expectations from 3.3% to 4.3%. CPI data indicated persistent inflation, with total CPI up 0.5% month-over-month and 3.0% year-over-year, while core CPI, excluding food and energy, rose 0.4% and 3.3%, respectively, raising concerns about the Fed’s ability to reach its 2.0% target. On the other hand, the January PPI report provided some relief, suggesting that key components such as airfares and physician services could help contain inflation. Retail sales data for January disappointed, and industrial production growth was primarily driven by increased utilities output due to cold weather rather than manufacturing or mining. Treasury yields edged lower, with the 10-year yield dipping one basis point to 4.48% and the 2-year yield dropping three basis points to 4.26%. For the week, the Dow gained 0.6%, the S&P 500 rose 1.5%, and the Nasdaq outperformed with a 2.6% increase.

Weekly Market Heatmap

Weekly Sector Performance

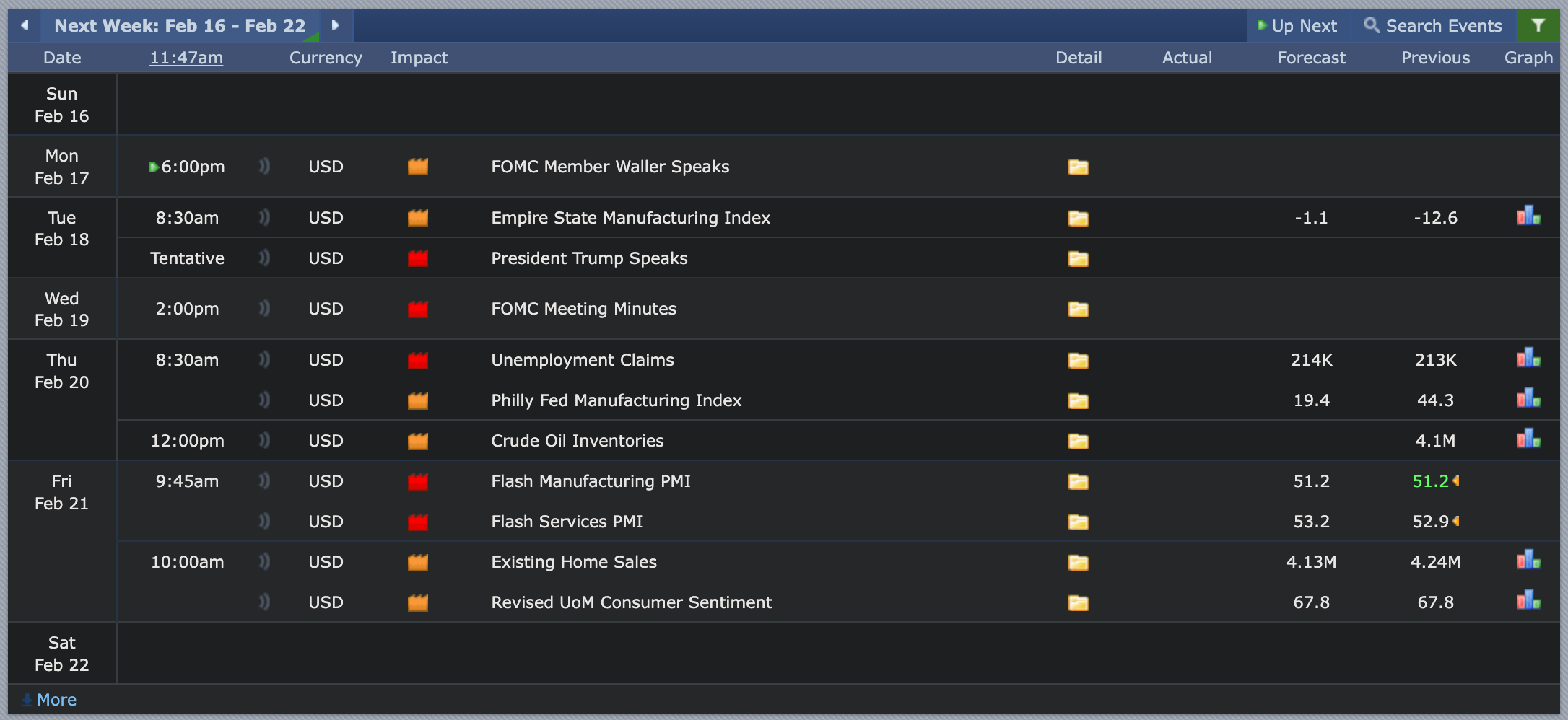

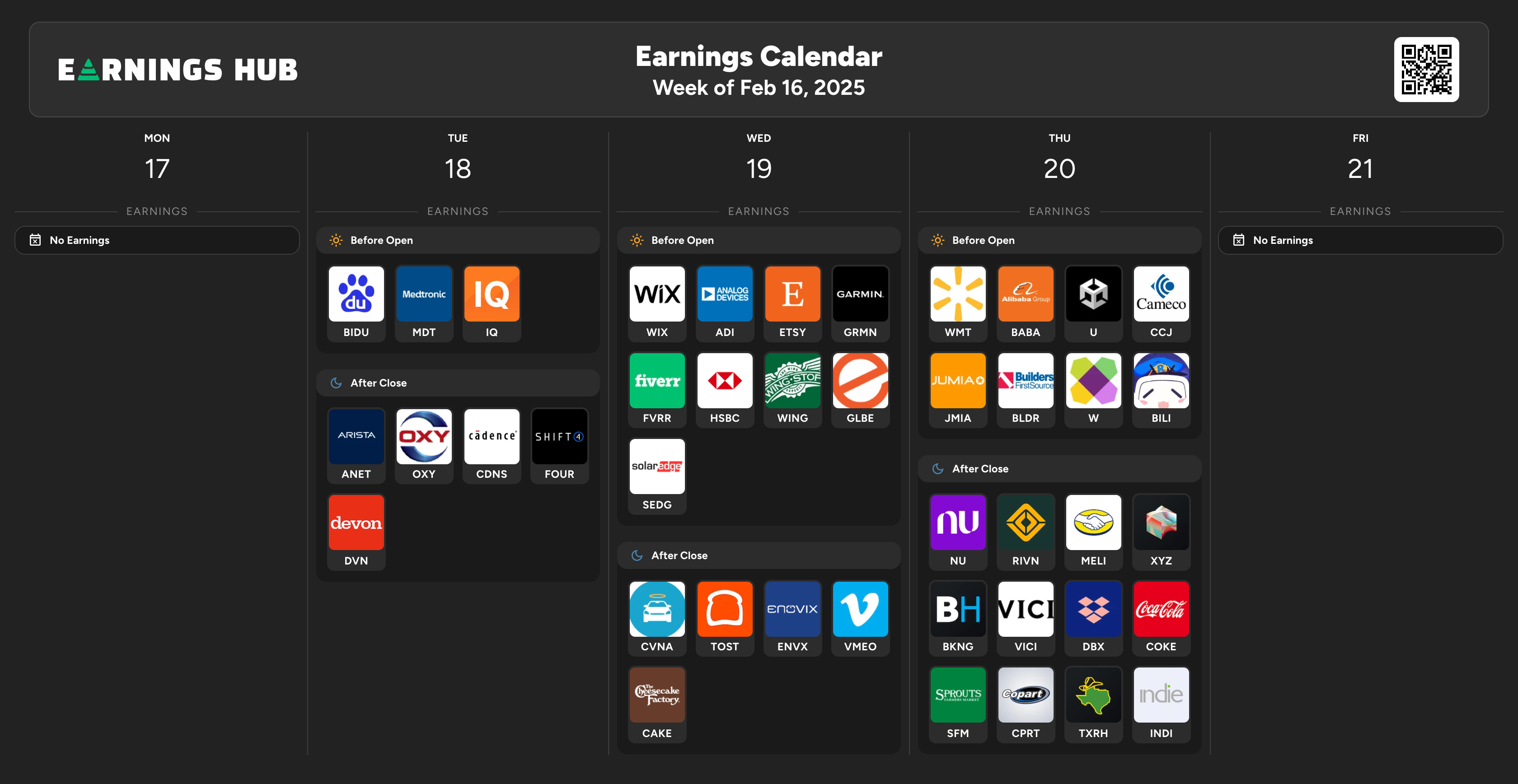

Looking Ahead to the Upcoming Week

Looking ahead to the week of February 16-22, 2025, markets will focus on key economic events and earnings reports. Notable economic releases include the Empire State Manufacturing Index on Tuesday, FOMC Meeting Minutes on Wednesday, and Unemployment Claims along with the Philly Fed Manufacturing Index on Thursday. Additionally, inflation data such as CPI and PPI readings will be closely monitored for insights into the Federal Reserve's monetary policy outlook. President Trump is also scheduled to speak, potentially impacting market sentiment. On the corporate front, major earnings reports will come from companies like Alibaba (BABA), Analog Devices (ADI), Medtronic (MDT), and Arista Networks (ANET), among others, providing insights into various sectors.

Mid-week volatility could arise from Fed-related developments and trade policy updates. The FOMC minutes release may offer further clarity on the central bank’s stance on interest rates, particularly after Powell’s recent comments about inflation concerns. Key earnings reports from tech and consumer-facing firms like Etsy (ETSY), Garmin (GRMN), and Shopify (SHOP) will shed light on consumer spending trends. Investors will also watch crude oil inventory data and housing market indicators such as existing home sales. With economic data, Fed updates, and earnings season in full swing, traders should brace for potential market swings and sector-specific movements.

Economic Events

Earnings Event

Market Health

The market is showing signs of weakness.

Broader Market - SPY, QQQ, IWM, MDY

The market is showing mixed signals with relative strength in large-cap stocks but weakness in small and mid-cap equities. The S&P 500 (SPY) and Nasdaq 100 (QQQ) are continuing their upward trend, with QQQ leading in gains, up +2.91% for the week, indicating strong momentum in mega-cap tech stocks. SPY also posted gains of +1.49%, suggesting continued buying interest in large-cap equities.

However, small-cap (IWM) and mid-cap (MDY) indices are underperforming. IWM (Russell 2000) is relatively flat for the week (-0.01%), struggling to gain upside traction, while MDY (S&P 400 MidCap) declined -0.24%, reflecting weakness in mid-sized companies. The divergence between large caps and smaller stocks suggests a narrower market rally, where investors are favoring mega-cap technology stocks over broader market participation.

Watch List

To be provided on X:

Disclaimer: This newsletter is not trading or investment advice, but for general informational purposes only. This newsletter represents our personal opinions that we share publicly for educational purposes. Futures, stocks, and bonds trading of any kind involves a lot of risks. No guarantee of any profit whatsoever is made. In fact, you may lose everything you have. So be very careful. We guarantee no profit whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission, CFTC, or with any other securities/regulatory authority. Consult with a registered investment advisor, broker-dealer, and/or financial advisor. By reading and using this newsletter or any of my publications, you are agreeing to these terms. Any screenshots used here are courtesy of ForexFactory, EarningsHub, Finviz, ThinkorSwim, and/or Tradingview. We are just end-users with no affiliations with them.