Market Trader Report V2#27

MyntBit's Market Trader Report brings potential setups for futures & stocks with a time horizon from days to weeks depending on price action. The following research is based on Fundamentals, Technical & Options Analysis.

What is included in this week's edition?

WEEKLY REVIEW: An overview of current market standing, fundamental matters with implications upon the market, and general sentiment regarding the major US indices.

LOOKING AHEAD: Key takeaways to consider as we look forward to the upcoming trading week.

FUTURES MARKETS: ES, NQ, RTY - A technical review of the major indices, futures, and commodities that represent the overall health of the market.

SPDR SECTORS & ETFs: SPY, QQQ, IWM - An in-depth review of the SPDR sectors with keynotes on market strength, opportunities, and relative rotation.

Market Trader by MyntBit

Weekly Review

Stocks had a positive week, with major indices experiencing decent gains. Some weaker price movements toward the end of the week were balanced by substantial gains earlier. The major indices had four consecutive winning sessions leading up to Wednesday. The S&P 500 moved above its 50-day moving average. Broad-based gains indicated a willingness to buy on weakness, helped by a drop in market rates. Mega-cap stocks performed well, with the Vanguard Mega Cap Growth ETF (MGK) rising 3.6% and the Invesco S&P 500 Equal Weight ETF (RSP) rising 2.3%.

Yields on the 2-year and 10-year notes fell in response to mixed economic data, signaling market hopes for no further rate hikes by the Fed. Economic data this week included the Consumer Confidence Index, JOLTS Job Openings Report, Q2 GDP estimate, Personal Income and Spending, ISM Manufacturing Index, and Employment Situation Report.

Oil prices had a significant but unnoticed increase, with WTI crude oil futures rising 7.8% to $85.55/bbl, boosting the S&P 500 energy sector. However, concerns about persistent inflation arose.

The information technology, consumer discretionary, and communication services sectors saw the largest gains, while the utilities and consumer staples sectors ended the week with losses. In earnings news, Salesforce performed well, while Dollar General and Five Below faced challenges. Best Buy and Lululemon Athletica reported positive results.

Note that equity and bond markets will be closed on Monday for Labor Day.

Weekly Performance Heatmap

Overall Stock Market Heatmap & Sector Performance

Looking Ahead to the Upcoming Week

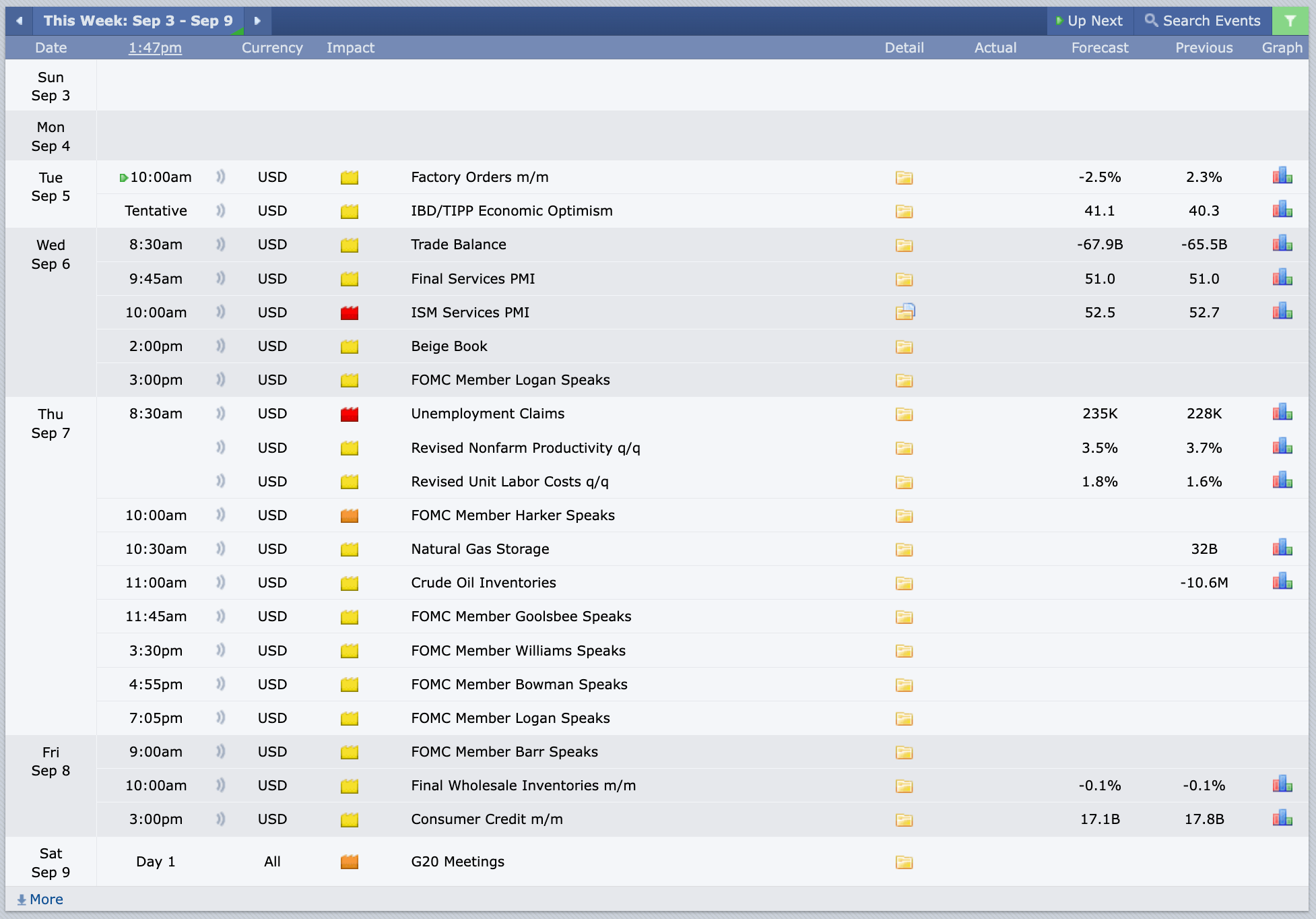

In the upcoming holiday-shortened week, key economic events include the release of August purchasing managers' reports for the service industry and the Fed's Beige Book regional survey.

Other data on the agenda includes July's factory orders, trade balance, and consumer credit, along with finalized July durable goods orders and wholesale inventories.

Asian markets will focus on Chinese inflation data, including the Consumer Price Index (CPI) and Producer Price Index (PPI). China will also release service and composite PMIs, trade balance data, and foreign reserves figures for August. Japan will provide finalized second-quarter GDP, composite and services PMIs, and various economic indicators for July. The Royal Bank of Australia will hold a policy meeting, and both Australia and South Korea will release second-quarter GDP and August inflation data.

In Europe, attention will be on finalized August services and composite PMIs for the Eurozone, as well as individual measures for the U.K., Germany, and France. Eurozone data will include finalized second-quarter GDP, employment figures, July PPI, retail sales, consumer expectations survey, and inflation expectations. Germany will release finalized August CPI, factory orders, industrial production, and trade balance data. France will provide July industrial production and trade balance figures, along with finalized second-quarter wage data.

Earnings Calendar & Economical Events